What is VWAP and why it matters institutionally

VWAP (Volume Weighted Average Price) is the average price weighted by volume — a benchmark used by institutions to judge execution quality. Price tends to mean-revert toward VWAP intraday; extensions beyond standard deviation bands often offer fade or continuation edges depending on zone.

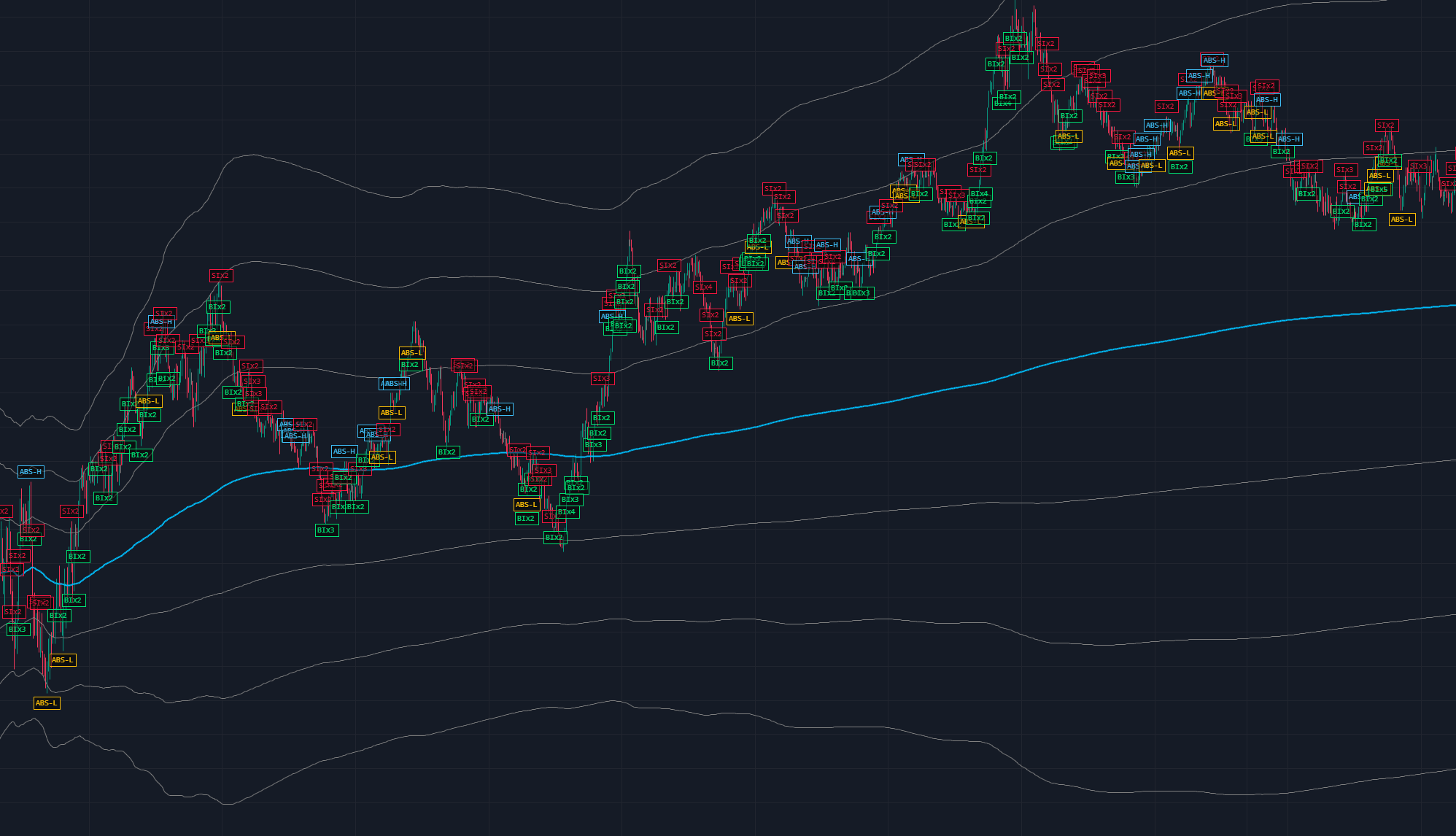

Standard deviation bands explained (1σ, 2σ, 3σ)

XtradeReverse plots VWAP plus/minus 1σ, 2σ, and 3σ bands based on session volume variance. Each band defines a statistical envelope — the farther price is from VWAP, the more extreme the short-term positioning.

The 16 VWAP zones in XtradeReverse

Zones combine side (above/below VWAP), band (inner, mid, outer, beyond), and direction (long/short permission). You enable only the zones where your strategy has historical edge — e.g. longs from -2σ to -1σ, shorts from +2σ to +3σ.

Which zones to trade long vs short

- Mean reversion: enable counter-trend zones (e.g. long below VWAP in negative σ bands)

- Trend continuation: enable zones in the direction of the session trend only

- Disable “beyond” zones until you understand volatility expansion risk

Session timing (GMT+8 configuration)

VWAP resets on session boundaries you define in trading sessions. For Asian session futures, align session start/end to GMT+8 (or your exchange local time) so bands reflect the correct volume profile. Wrong session reset is a common reason filters feel “too strict” or “too loose.”